Cybersecurity for Insurance AI: 2026 Risk Manager’s Guide

Cybersecurity for insurance AI is defined as the full set of controls, processes, and governance measures that protect artificial intelligence systems and the sensitive data they process within insurance operations, covering underwriting automation, claims processing, and fraud detection. The NAIC holds insurers responsible for compliance and fair treatment even when AI vendors make the underlying decisions, which means cyber risk management for insurance is no longer a back-office IT concern. It sits at the center of regulatory accountability, vendor oversight, and operational integrity. Insurance professionals who treat AI security as optional are, in practice, accepting liability they cannot price.

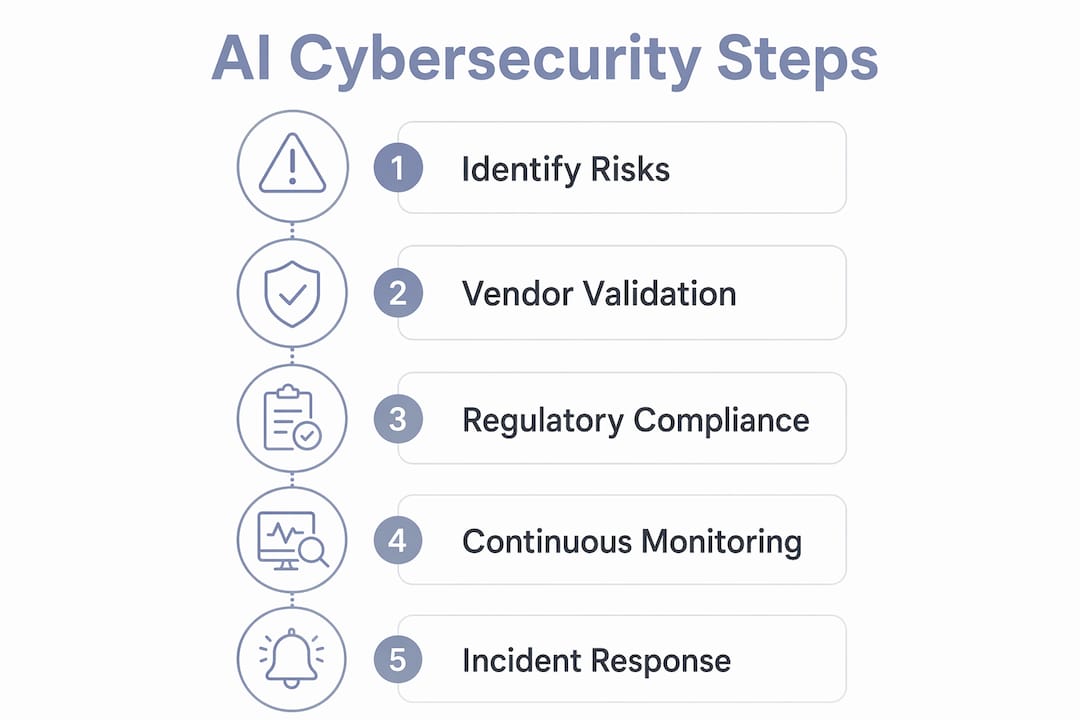

What are the core cybersecurity risks of AI in insurance?

AI systems in insurance handle some of the most sensitive personal data in any industry: medical histories, financial records, and behavioral profiles. Expansion of AI use intensifies personal data flows and raises the blast radius of any breach, making AI-specific security mandatory rather than optional. Traditional perimeter defenses were built for static systems. AI models introduce a different attack surface entirely.

The risks fall into three distinct categories:

- Data breaches in AI-driven workflows. Underwriting and claims tools ingest policyholder data continuously. A compromised model or misconfigured API can expose thousands of records before any alert fires.

- Model failures and biased outputs. An AI model that produces discriminatory pricing decisions creates both regulatory exposure and reputational damage. The failure mode is not always a hack. It can be a drift in training data or a corrupted update.

- Supply-chain and third-party vendor exposure. Most insurers do not build their own AI models. They buy or license them. AI accelerates cyberattack timing and complexity, and attackers now target the vendor layer specifically because it gives them access to multiple carriers at once.

Pro Tip: Map every AI vendor in your stack against the data categories they touch. If a vendor processes protected health information or financial data and holds no SOC 2 Type II certification, that is an open risk item, not a future agenda point.

The speed dimension matters here. Attackers use AI to probe defenses faster than human security teams can respond. Supply-chain exposure and contingent business interruption have moved from theoretical risk categories to active underwriting conversations at major carriers.

How do regulatory frameworks shape insurance AI cybersecurity?

Regulation is the most concrete forcing function for AI security investment in insurance. The rules are specific, the timelines are firm, and the penalties for non-compliance are material.

- NAIC Model Bulletin on AI. The NAIC has established that insurers bear direct responsibility for the decisions their AI systems produce, regardless of whether a third-party vendor built the model. Human oversight is not a best practice. It is a compliance requirement.

- EU AI Act, effective August 2026. The EU AI Act requires auditable documentation of AI-assisted underwriting decisions, including bias testing and explainability records. US carriers operating globally are already adapting their governance frameworks to meet this standard.

- State-level privacy and AI laws. Several US states have enacted or proposed AI-specific regulations targeting insurance pricing and claims automation. Colorado’s SB 21-169 on algorithmic discrimination in insurance is one example. Carriers must track a patchwork of requirements across every state where they write business.

- Documented AI governance and evidence retention. Regulators increasingly ask for proof, not promises. Audit trails, model version histories, and incident logs must be retained and retrievable on demand.

The practical implication is that cybersecurity for insurance AI is inseparable from compliance. A carrier that cannot explain how its fraud detection model reached a decision is exposed on two fronts simultaneously: a potential regulatory violation and a potential security gap. Both require the same underlying infrastructure of documentation and control.

What are best practices for assessing AI vendor cybersecurity risks?

Vendor selection is where most insurance AI security failures originate. A carrier can have excellent internal controls and still be fully exposed through a vendor that processes its data without adequate protections.

| Evaluation Criterion | What to Verify |

|---|---|

| SOC 2 Type II certification | Confirm scope covers AI training and inference environments, not just generic IT infrastructure |

| ISO 27001 certification | Check that the certification applies to the specific systems handling your policyholder data |

| Model isolation | Verify dedicated infrastructure per client to prevent cross-client data leakage and protect proprietary underwriting logic |

| Explainability and provenance | Require documentation showing how the model reaches decisions and where its training data originated |

| Incident response plan | Confirm breach notification timelines meet state requirements, typically 30 to 72 hours depending on jurisdiction |

SOC 2 Type II and ISO 27001 certifications need operational scope demonstrating data security specifically for AI training and inference environments. A vendor who presents a certificate covering their email servers but not their model training pipeline is offering you paper, not protection.

Model isolation deserves particular attention. Dedicated infrastructure per client prevents cross-client data leakage and protects proprietary underwriting logic from competitive exposure. If your vendor runs multiple carriers on shared infrastructure, your pricing models and risk selection criteria are potentially visible to competitors.

Pro Tip: During vendor due diligence, ask for a live demonstration of their incident response process, not just a written plan. Request the last tabletop exercise report. Vendors who cannot produce one have not tested their response capability.

Understanding AI security at every lifecycle stage is the foundation for asking the right questions during procurement. Most vendor assessments focus on the deployment phase. The training and fine-tuning phases carry equal or greater risk.

How is cyber insurance evolving in response to AI risks?

The cyber insurance market is experiencing a tension that directly affects every insurance professional reading this. Carriers are being asked to price and cover AI-driven risks that are evolving faster than actuarial models can track.

- Cyber carriers report a negative rate environment lasting roughly three years, with gradual stabilization beginning in 2026. Soft pricing has persisted even as the underlying threat severity has increased, creating a structural mismatch between premium and exposure.

- Munich Re confirms that typical cyber policies cover non-physical damage from both malicious and non-malicious events. This matters for AI specifically because model failures and unintentional data exposures fall into the non-malicious category that many policyholders assume is excluded.

- Business interruption coverage tied to AI system failures is becoming a standard discussion point in policy renewals. A claims processing AI that goes offline for 48 hours represents a quantifiable revenue loss, not just an IT inconvenience.

- Incident readiness is now a pricing factor. Munich Re’s position is that cyber insurance helps clients understand and mitigate risks proactively, not just compensate after loss. Carriers with documented AI security programs are beginning to see that reflected in their own coverage terms.

The market signal here is clear. Insurers who underwrite cyber risk for others must also demonstrate that their own AI operations meet the security standards they require of their policyholders. The credibility gap between what carriers demand from clients and what they practice internally is closing, driven by regulatory scrutiny and reinsurer requirements.

What practical steps can risk managers take to secure AI workflows?

Allianz manages AI security as an end-to-end operating model requirement, integrating continuous monitoring and risk assessment throughout the AI lifecycle rather than treating security as a point-in-time check. That model is the right one, and it is replicable at carriers of any size.

Here is what practical implementation looks like for a risk manager:

- Embed security in the AI procurement process. Security review should happen before a vendor contract is signed, not after deployment. Build a standard AI vendor security questionnaire and make it a procurement gate.

- Implement continuous monitoring for AI systems. Static annual audits do not catch model drift, data poisoning, or unauthorized access patterns. Automated monitoring tools that flag anomalies in model behavior or data access are now accessible to mid-size carriers.

- Align AI governance with regulatory timelines. The EU AI Act’s August 2026 deadline is not a distant concern for US carriers with international operations. Build explainability and audit trail requirements into your AI governance framework now.

- Train human operators alongside AI systems. End users in AI safety are a critical and often underestimated control layer. Phishing attacks and social engineering attempts targeting employees who interact with AI systems are a documented attack vector.

- Practice incident response specific to AI failures. A general IT incident response plan does not cover the specific steps required when an AI model produces discriminatory outputs or when training data is exfiltrated. Develop AI-specific runbooks.

Pro Tip: Establish a cyber hygiene baseline for every team that interacts with AI systems, including underwriters and claims adjusters who use AI-assisted tools. Human operators are frequently the entry point for attacks targeting AI workflows.

Proactive AI security risk management enhances customer trust, supports regulatory compliance, and reduces costly disruptions. The carriers that treat AI cybersecurity as an operational mandate rather than a compliance checkbox will carry a measurable competitive advantage as regulatory scrutiny intensifies.

Key takeaways

Cybersecurity for insurance AI requires continuous vendor validation, regulatory alignment, and lifecycle-integrated controls to protect sensitive policyholder data and maintain operational integrity.

| Point | Details |

|---|---|

| Define the scope clearly | Cybersecurity for insurance AI covers underwriting, claims, fraud detection, and every vendor that touches those systems. |

| Vendor certification is not enough | SOC 2 Type II and ISO 27001 must cover AI training and inference environments specifically, not just general IT infrastructure. |

| Regulation is a security driver | NAIC accountability rules and the EU AI Act require documented explainability and audit trails as baseline compliance. |

| Cyber insurance pricing is shifting | Soft market conditions are stabilizing as AI-driven threat complexity forces carriers to reassess risk models and incident readiness. |

| Human operators are part of the attack surface | Training staff who interact with AI tools is a security control, not a soft skill exercise. |

Why the industry is still underestimating this problem

I have spent enough time working at the intersection of AI systems and security to say this plainly: most insurance organizations are treating AI cybersecurity as a vendor problem. They assume that if the vendor has a certificate, the risk is managed. That assumption is wrong, and it is going to cost carriers real money.

The attack surface for an AI-driven insurance operation is not the same as a traditional IT environment. Prompt injection attacks, data exfiltration through model outputs, and supply-chain compromises targeting AI training pipelines are not covered by the security frameworks most carriers have in place. The OWASP Top 10 for LLM Applications exists precisely because these risks require a different taxonomy.

What I find most concerning is the gap between how carriers assess cyber risk in their policyholders and how they assess it in their own AI operations. A commercial lines underwriter will ask a manufacturing client detailed questions about their OT security posture. That same carrier may have deployed three AI tools in the past 18 months with no model isolation verification and no AI-specific incident response plan.

The regulatory window for voluntary compliance is narrowing. The EU AI Act deadline is August 2026. State regulators are watching how carriers respond. The carriers who build genuine AI security programs now will be better positioned when the first major AI-related enforcement action lands. And it will land.

— Nicholas

How Thepitstop can strengthen your insurance AI security posture

Insurance professionals managing AI risk need tools that match the actual threat surface, not generic IT security checklists. Thepitstop is built specifically for securing AI agents and the human operators who work alongside them. The free AI Agent Security Scan gives risk managers an automated baseline assessment of their AI systems’ attack surface, covering prompt injection exposure, data exfiltration risks, and supply-chain vulnerabilities. For a deeper look at where liability gaps exist in AI-driven operations, the AI Agent Liability Gap white paper maps the specific coverage and governance failures that leave insurance carriers exposed. Both resources are free and built for professionals who need answers, not sales decks.

FAQ

What is cybersecurity for insurance AI?

Cybersecurity for insurance AI is the set of controls, governance processes, and monitoring practices that protect AI systems used in underwriting, claims, pricing, and fraud detection from cyber threats, data breaches, and misuse. The NAIC holds insurers directly accountable for the decisions these systems produce, regardless of whether a third-party vendor built the model.

What certifications should an AI vendor hold for insurance use?

AI vendors should hold SOC 2 Type II and ISO 27001 certifications, but the scope must explicitly cover AI training and inference environments. A certificate that applies only to general IT infrastructure does not address the specific risks of handling policyholder data in model training pipelines.

How does the EU AI Act affect US insurance carriers?

The EU AI Act, effective August 2026, requires auditable documentation of AI-assisted underwriting decisions, including bias testing and explainability records. US carriers operating in European markets or using EU-based vendors must adapt their AI governance frameworks to meet these requirements.

What does cyber insurance cover for AI-related incidents?

Standard cyber policies cover non-physical damage from both malicious and non-malicious events, which includes AI model failures and unintentional data exposures. Munich Re notes that coverage increasingly extends to business interruption caused by AI system outages, with incident readiness becoming a factor in policy pricing.

How should risk managers respond to an AI-related security incident?

Risk managers need AI-specific incident response runbooks that address model failures, discriminatory outputs, and data exfiltration separately from standard IT incidents. Breach notification timelines under state law typically range from 30 to 72 hours, and documentation of the AI system’s behavior before and during the incident is required for both regulatory reporting and insurance claims.